The Amazing Power of an Advance Payment

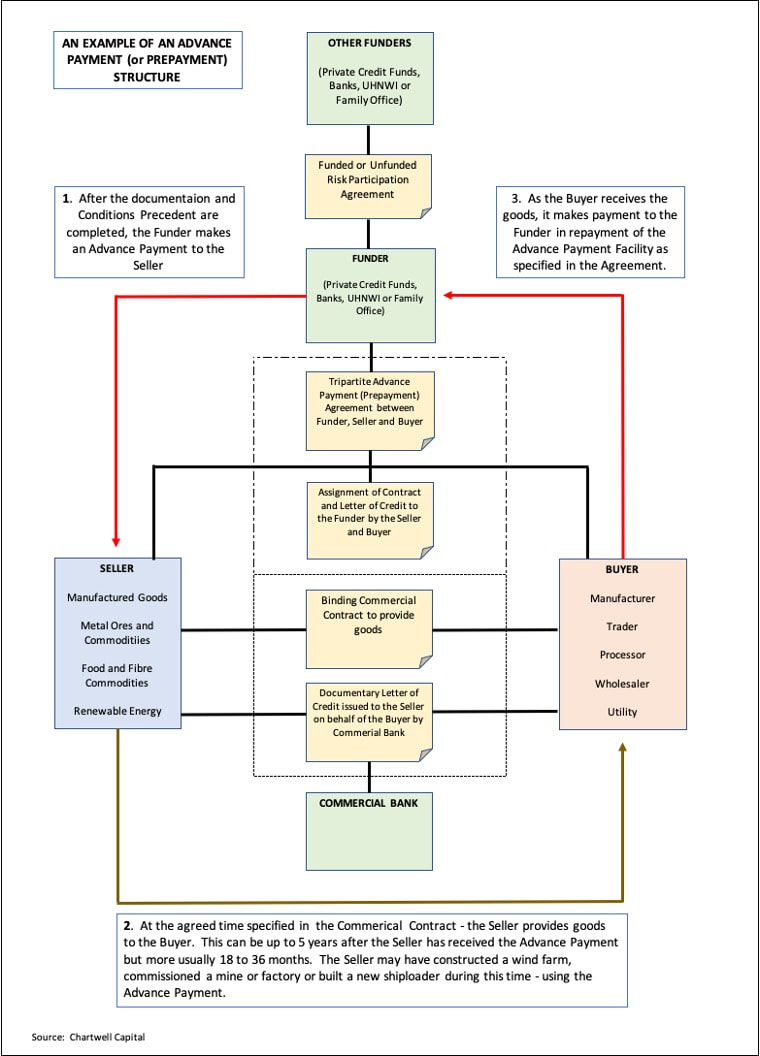

(Often called a Prepayment) Problem: You want to do a brownfield expansion of your mine or install some new capital equipment to expand production. Unfortunately – your banker either doesn’t understand your request – or can’t get an approval from their credit department. And your shareholders don’t want to dilute their equity by raising more capital. Solution: You negotiate a long-term offtake contract with your preferred Buyer. The value of the goods or minerals to be delivered over the term will pay for the investment you want to make. Then you talk to a private credit fund or an investor through your preferred consultant and negotiate a three-way Advance Payment Agreement. You also pay some money to some lawyers to document everything. The Funder makes payment now to you for the goods or minerals you are going to deliver in the future. Benefits: All parties win – the Seller uses the Advance Payment productively. The Buyer has a locked in supply contract from a preferred Seller. The Funder makes a margin on the funding. If well structured – this arrangement can also often be classified as a trade payable/receivable – not core debt. Your CFO and Treasurer will like this. Other Sectors: Though most often used with bulk commodities such as wheat, refined energy products or metal ores, this structure has also been used to fund the construction of wind and solar farms and for commercial construction. The Seller and the Buyer need to have a strong and trusting relationship. Next Steps: When well designed, an Advance Payment or Prepayment is an amazingly powerful tool to source capital and enhance liquidity quickly. We have originated and designed prepayments that have provided clients with $100's of millions of funding over the last few years. Contact us for a confidential initial conversation to see what is possible. David L Thomas 13 June 2023

0 Comments

In a previous life I spent some time as State Manager for the Australian Government owned Australian Wheat Board - which then had a legislated monopoly on the marketing rights for Australia’s export wheat crop. This arrangement was deregulated long ago and I returned to banking before that happened. Back then - and still now - I regularly download the monthly USDA World Food Outlook - the so called WASDE. In the light of a report in the FT outlining the dire situation emerging for food security in many countries right now as a result of the #ukrainerussianwar -the data from the most recent WASDE on 9th March is interesting . In a nutshell - the USDA estimates that in 2022 total traded wheat this year will be 203.1 million tonnes - assuming Russia and Ukraine can export their usual crops due from the spring planning season in a few weeks. USDA estimates that Australia will export 23.85 million tonnes of wheat this year - so 11.74%. This won’t fill the gap left by the absence of Ukraine and Russian grain - which usually supplies between 20 and 30% of globally traded wheat. The pressure will be on the US, Canada and Latin America to fill the gap. They haven’t had a good season so far due to drought across a lot of the Americas - so it’s a difficult time for world grain supply. It’s going to be a volatile food security environment over the next few months for many governments who are net grain importers. With wheat futures enabling some Australian wheat growers to lock in a price of A $ 500 tonne or more right now - according to Malcolm Bartholomaeus - there’s lots of head scratching and discussions with farm advisors and consultants about the plan for the coming Australian winter crop grain planting season which usually starts in late April with the arrival of the winter rains. This is an amazing price compared to recent history. The problem is - as reported by Liv Casben - cropping input costs have also risen - due to the #ukrainerussianwar some fertilisers are now 3 times the price of last year - and diesel is double the price So what to do if you are a farmer? It comes down to a hard nosed assessment of return on costs. Wayne Pluske has some good models to look at in this report from the Australian Farm Weekly. Some farmers I know will stick to their cost budget - and therefore reduce the size of their planting. Others will dramatically cut back on fertiliser application and hope the yield penalty won’t be too harsh. And some may well decide to sit out this year - especially if they don’t have a large farm debt to service. Who’d be a farmer? David L Thomas 22 March 2022 An earlier version was posted on LinkedIn on 21 March 2022:  I was chatting to the plumber who had come to fix the taps to our outdoor shower last week. It was a quick job - maybe 30 minutes - but in that time he established that I work in finance and banking. He told me he had just invested thousands of Australian dollars into Bitcoin and Ethereum through an app on his mobile phone – and proudly showed me his gains – up 15% since his investment earlier in the week. He wanted to know if he had done the right thing. Put on the spot – I said that if it was money he could afford to lose – no more than 5% of his investable assets – it was probably ok to dabble. But I stressed that it was just pure speculation – gambling really. Taking a punt. He’s not alone. A survey by Finder – summarised by Sebastian Sinclair in CoinDesk in October 2021 - found that Australians were the third highest holders of crypto currencies globally – with 18% of the population owning crypto. Bitcoin was the most popular, followed by Ethereum. And it’s not just the Australian plumbers diving in. The global club of billionaires are increasingly adding cryptocurrency to their portfolios. Scott Carpenter reported in January 2022 that crypto sceptic and billionaire fund manager Thomas Peterffy is now recommending his clients invest 2 to 3 percent of their net wealth in crypto – just in case fiat currency “goes to hell.” Of course, as in all endeavours – there are good and bad actors. In the world of crypto there is evidence of criminal behaviour – some sponsored by state actors. A recent evidence trail points to significant payments in bitcoin from outside the US to activists associated with the January 6 capital riots in Washington last year. Meanwhile, in their fascinating 2022 note lead authored by Gabriel Soderberg - Behind the Scenes of Central Bank Digital Currency – the IMF explores the actions of many central banks considering the use of central bank digital currency (CBDC) – or legal crypto (exchangeable for fiat or as actual fiat currency). The note looks at the case studies in the Bahamas, Canada, China, the Eastern Caribbean Currency Union, Sweden, and Uruguay. The Bahama’s have already issued a retail CBDC – called the Sand Dollar. There are good reasons for central banks to consider a digital currency – including promoting an increase in financial inclusion, improving access to payments by people who don’t have bank accounts, filling gaps in payment needs that are being vacated by commercial banks and reducing risks of financial crime. The study also points to reasons for concern. Concerns include the potential loss of anonymity associated with traditional cash. The Reserve Bank of Australia is well advanced with a trial of its own Central Bank Digital Currency – in partnership with Commonwealth Bank, National Australia Bank, Perpetual and ConsenSys Software. Dharmesh Mistry warns that the commercial banking world needs to get on board with and understand crypto. It could be the tsunami that will blow away their franchise. Especially as Facebook leads the charge by the tech majors into the Metaverse – with parallel worlds of value and massive inbound funds flow as people acquire virtual assets such as NFT artworks and virtual real estate. As we survey the legitimate and speculative crypto universes – here’s two warnings from commentators I respect: Yanis Varoufakis in January 2022 on Facebook’s Metaverse and entering the kingdom of Zuckerberg: “Zuckerberg’s ambition is to insert his billions of Facebook non-gamer users into a Steam-like digital social economy – complete with a top-down platform currency that he controls. How can I resist the parallelism with a digital fiefdom in which Zuckerberg dreams of being the techno-lord?” And Leda Glyptis – musing about the dystopian future of money in a digital world at Sibos 2021: “Because digital currencies are effectively programmable money. And you know what that means? That means it will be possible for the issuer of the programmable currency to make it impossible to spend in certain ways. In certain industries. In certain countries. Gambling. Alcohol. It will be possible to make it impossible for you to pay for a luxury item, or perceived luxury item, a holiday, or a new car before you have paid your child support or your taxes or your rent. It may be impossible for you to spend your money in France or Bolivia. Oh, come on now, I hear you say. Why would anyone do that? Because the vast majority of regimes are illiberal. Because even liberal regimes have short-term goals that need to be met and the means sometimes feel, rightly or wrongly, sanctified by the aims.” So - what’s the so what? How do professionals engage with crypto and digital currency? Two suggestions:

By David L Thomas, 12 March 2022 11/2/2020 0 Comments Sustainable Value MetricsUsing Sustainable Value Metrics to access sustainable and green finance

There is a lot of green and sustainable debt capital available On 8th January 2020, BloombergNEF reported[1] that sustainable debt finance issued during 2019 rose 78% during 2019 to over USD 465 billion . This is a vast and rapidly growing pool of capital being directed by investors, funds and banks towards green and sustainable debt finance. Most of this was in the form of Green Bonds (over USD 260 billion issued in 2019) and the pace of issuance of green bonds is predicted to accelerate further - with Lombard Odier predicting in January 2020 that the global green bond market to expand again to USD 320 billion during 2020[2]. This prediction may prove to be too cautious given the pace at which investible Green and Sustainable bonds and debt capital pools are being created. A good early example in 2020 was the issuance of a EUR 300 M green covered bond on Monday 20th January by the European bank group Nord/LB under Luxembourg law[3]. This was the first issuance of a green covered bond under the amended Luxembourg Pfandbrief Act for “Lettres de Gage” (2018) – with proceeds dedicated to green financing of wind energy and solar projects. If you are curious to see how the bond works – work through the prospectus and compliance documentation supporting this issuance – available from the Luxembourg Stock Exchange[4]. Why should I be interested in the growth in green and sustainable debt funding? There are several reasons - and running across all of them is an increasing sense of urgency by investors, communities, governments and regulators to address the need to invest in the global economy’s transition to a low carbon economy. Funding is being redirected towards sustainable outcomes and priorities. Don’t leave yourself or your business starved of capital by ignoring what’s happening. First reason: ESG is now mainstream “ESG” usually means “Environment, Society and Governance” - though I have seen variations on these terms. Essentially, it’s about understanding, measuring and improving the impact of your company operations on the environment and communities you operate in. Understanding ESG is now a basic hygiene factor around a corporation’s license to operate in a community – and this understanding is a core competency for company directors and managers. Most ESG compliance frameworks require a company to first set KPI’s around its ESG objectives and then to measure and report against these objectives. Many ESG frameworks draw from and reference the 17 United Nations Sustainable Development Goals (SDG’s)[5]. Building from the SDG’s there are now many different frameworks and tools available to assist implementing a robust ESG framework. A good place to start is the ESG Disclosure Handbook [6] and other material published by the World Business Council for Sustainable Development. Providers of debt capital (banks, venture capital funds, pension funds and other investors) are saying that they now require their borrowers to have a high ESG rating in order to attract a loan. Why is this? Because their investors and depositors – both large and small - are demanding that their money is deployed towards sustainable investments and business activities. A recent global survey of over 25,000 retail investors by Schroders found that the majority of investors in Asia (73% in India; 66% in China) are actively directing their investments into high ESG rated investments[7]. So, to maintain alignment with their depositors and investors – banks and other providers of debt capital are now packaging it into product channels for deployment – mostly into green loans and bonds and sustainable finance lending. You’ll only get access to this debt capital if you can demonstrate a strong understanding of ESG in your business, can report on your ESG footprint to your bankers and other stakeholders (especially customers and shareholders) and your use of the capital (green loan or sustainable finance) will further improve your ESG rating (for example – your green loan may be to enable you to invest in renewable energy systems that will reduce your emission of greenhouse gases). Second Reason: Regulators are now focussing on the business and economic risks arising from climate change Most advanced economies have regulators that operate independently (or semi independently) from the government of the day. There are many types of regulators – but the most important for the financial system and the economy are usually the central bank (in Australia that’s the Reserve Bank), the corporate regulator (in Australia that’s ASIC - the Australian Securities and Investment Commission) and the bank and insurance regulator (in Australia that’s APRA – the Australian Prudential Regulation Authority). It’s the job of the regulators to try to maintain economic stability and reduce the adverse impacts of financial risks to the economy – these risks ranging from financial crime to adverse economic cycles and external shocks such as the current corona virus outbreak in China. The Bank of International Settlements (BIS) is effectively the global central bank regulator – with most advanced economies as members. The BIS makes recommendations – that are usually adopted – about how each country should manage its banks and other financial system operators to maintain economic stability and reduce the impact of economic shocks. In January 2020 the BIS released a paper called The Green Swan: central banking and financial stability in the age of climate change.[8] It’s a fascinating read – and get ready for its recommendations to filter through to the thinking of your local central bank and other local regulators. Quoting from the paper’s abstract: Central banks can therefore have an additional role to play in helping coordinate the measures to fight climate change. Those include climate mitigation policies such as carbon pricing, the integration of sustainability into financial practices and accounting frameworks, the search for appropriate policy mixes and the development of new financial mechanisms at the international level. In Australia right now, despite the fact that the government of the day is reluctant to accept the economic impact of climate change, the regulators are getting on with trying to deal with the economic risks of climate change anyway. Australia’s APRA published a discussion paper[9] on climate risk in March 2019 summarising its view of climate risk and referencing the work it was doing to monitor and reduce the risks to the financial system from climate change – including enhanced supervisory action and domestic regulatory coordination and development of climate change analytical tools. Similarly, Australia’s ASIC is now busy issuing regulatory guidance on climate change risk based on guidelines issued by the G20 Financial Stability Board’s Taskforce on Climate Related Financial Disclosures (TCFD) . Third Reason: Your shareholders will demand it. At the BP annual general meeting in Scotland on 21 May 2019, 99% of shareholders supported a binding resolution filed by shareholders acting as the Climate Action 100+ group requiring the company to adopt a business strategy consisted with the goals of the Paris Agreement on climate change[10]. This was after a long and bitter campaign over several years by activists. These actions are gaining momentum and company directors can no longer regard climate concerns as being from the fringe. Climate concern is mainstream and company owners and directors are foolish to pretend otherwise. How do I access Green and Sustainable Finance? Develop your Sustainable Value Metrics The most important thing is to sit down and work out how to adapt your business to focus on the generation of Sustainable Value and work out how to measure the Sustainable Value your business is creating for your shareholders and stakeholders. If you can articulate your vision for creating Sustainable Value, describe how you measure it and how you report it – and the difference you are making in moving your company and your people to a sustainable business footing - you will be able to access the new pools of debt capital piling up to help you do this. This work is an extension of the ESG frameworks that have been developed around the world over the last ten years and already in use in many applications. However, there are so many ESG standards and frameworks it can be hard to navigate through the forest. One of the most positive developments from the recent World Economic Forum (WEF) in Davos was the release in January 2020 of the Consultation Draft Paper - Towards Common Metrics and Consistent Reporting of Sustainable Value Creation[11]. This paper has done a brilliant job of integrating the existing regulatory and voluntary ESG frameworks in place in global financial and investment markets and proposes a unified set of 22 Sustainable Value KPIs and reporting standards that are clear and applicable within most global corporate reporting and accounting systems with International Financial Reporting Standards (IFRS). Importantly – the 22 measures relate back to the themes of the SDG’s under the four pillars:

The Consultation Draft sets out a set of 5 criteria to assess the proposed themes and metrics recommended. The January 202 WEF Sustainable Value Framework is an excellent template to use to start to develop your Sustainable Value Metrics. I think you will find it easier than you may initially think – a lot of the measures proposed are already in common use in business and accounting frameworks. Once you have developed your Sustainable Value Metrics – then you will be equipped to hold a conversation with your advisors and your bankers about how you are going to apply green and sustainable debt capital to contribute to a sustainable future. David L Thomas February 2020 [email protected] [1] https://about.bnef.com/blog/sustainable-debt-sees-record-issuance-at-465bn-in-2019-up-78-from-2018/ [2] https://www.lombardodier.com/contents/corporate-news/investment-insights/2020/january/cio-viewpoint-how-to-invest-in-a.html?skipWem=true [3] https://www.nordlb.com/nordlb/press/press-release/nordlb-cbb-successfully-issues-green-covered-bond-on-the-capital-market-for-the-first-time/ [4] https://www.bourse.lu/security/XS2079316753/301122 [5] https://www.un.org/sustainabledevelopment/sustainable-development-goals/ [6] https://docs.wbcsd.org/2019/04/ESG_Disclosure_Handbook.pdf [7] https://www.theedgemarkets.com/article/lead-story-asian-investors-most-keen-sustainable-investing [8] https://www.bis.org/publ/othp31.pdf [9]https://www.apra.gov.au/sites/default/files/climate_change_awareness_to_action_march_2019.pdf [10] https://www.iigcc.org/news/climate-change-resolution-at-bp-agm-from-climate-action-100-investors-passes-with-over-99-shareholder-support/ [11] https://www.weforum.org/whitepapers/toward-common-metrics-and-consistent-reporting-of-sustainable-value-creation to edit.  A year ago I sat down with my son Julian Thomas and did some focussed research with the objective of trying to identify the attributes which would be necessary for successful investment into broad acre farming in Australia. We were curious about whether Australian broad acre farming would be a stable and attractive asset class to investors - both to ourselves as small private investors - and also whether the asset class would appeal to large global and institutional investors. We collated some of our research into a paper, which had the following executive summary:

Attributes of successful investment into Australian broad acre farming The medium and long-term prospects for Australian agriculture are fundamentally positive, but the sector as a whole faces several key challenges in securing future prosperity. A growing global population and increased demand for high-quality product creates a strong demand which we are well positioned to fill. Australian agriculture is highly efficient, and at present Australia has a comparative advantage in primary production. Low average returns disguise the reality that many farms are poorly run or minimally viable – the clear majority of total Australian agricultural output derives from a tiny minority of top-performing farms with excellent and reliable annual returns, which at scale is potentially highly attractive to international investors. Like many human activities, agriculture contributes to global climate change. However more sustainable production techniques assist in mitigation of these effects. In the absence of a market price on carbon emissions and other environmental mismanagement, or of widespread adoption of international standards for sustainable development, the short-term interests of farmers are misaligned with medium- and long-term continued productivity growth. Given an increasing government and community focus on sustainability, future opportunities exist for lucrative public/private partnerships around natural resource management which have yet to be fully explored. With shrinking rural populations, the availability of skilled labour is a potential limiting factor. This problem will be further exacerbated by the increased knowledge and skills threshold to engage with future agricultural technology, however operators are reluctant to invest in upskilling their often seasonal and temporary workforce, instead relying on temporary contractors to fulfil key roles. This ‘hollowing out’ issue is covalent with decreasing public sector investment in agricultural R&D and vocational education, leading to a decline in the renewal and growth of agricultural innovation and educational curricula and investment. With most of the land suitable for broad acre farming already under production, future prosperity will derive from embracing agricultural technology and sustainable development, the two key areas the top performers are already embracing and heavily investing in. A lack of public spending in this area has been mitigated to an extent by increased private sector investment, but such investment is usually limited to refinement rather than ‘blue sky’ innovation. It is likely that the key technologies behind future productivity increases will be: 1. Precision monitoring and information systems, enabling farmers to make smarter decisions faster; 2. Continuing the automation trend, driving up productivity and driving down expenses by freeing human operators from routine tasks; 3. Incorporating cutting-edge advancements in crop nutrition, bio genetics and selective breeding into routine farming operations, increasing yields with every generation; and 4. Tailoring machinery requirements and farm operations to each operation through bespoke hardware and software, driving increased productivity and enabling radical approaches to capturing all possible outputs for profit. We conclude that successful investment in Australian broad acre agriculture should therefore have the following attributes: 1. SCALE: Sufficient scale to maximise capital and process efficiency. 2. INNOVATION LED: Be innovation driven through by integration of network based skills and technologies that are applied actively and developed quickly at micro farm level and then multiplied across the business. 3. SUSTAINABLE AT THE CORE: Be sustainable, be in sync with community; and embrace all potential opportunities for revenue generation offered by the land footprint occupied, including carbon, water and energy. 4. BUILDING HUMAN CAPITAL AND BRAND VALUE in FOOD AND LAND MANAGEMENT: Actively embracing the opportunity to overcome the Australian and global skills shortage in agriculture through repositioning food production and land management as an innovative and vital sector full of opportunity. Looking back a year later, I think we would draw the same conclusions. Australian broad acre agriculture has strong potential, if investors are willing to engage through an investment framework that carefully deals with the above issues and with sufficient scale. In particular - the skills shortage must be comprehensively addressed for investors to be able to maximise the potential. And in addition - investors need to be embracing sustainability and technology as key enablers of productivity. By David and Julian Thomas Also posted on LinkedIn. An edited version of this post was published on www.graincentral.com on 6th April 2017 11/2/2017 0 Comments Step away from the puzzle I’ve become quite fond of jigsaw puzzles. Not the run-of-the-mill cardboard ones with regular shapes and twee pictures. I get puzzles shipped from Liberty Puzzles in the USA. They are made from high quality maple wood veneer and are laser cut into irregular shapes that fit together tightly. The pieces are tactile to hold and smell faintly of wood smoke from the laser cutting. The puzzles include pieces that Liberty call “follies” – which are puzzles within the puzzle with another narrative – usually related to the puzzle picture.

Because I am fond of fine art painting I usually choose a picture by a good painter. This one is Vanity, by Frank Cowper – painted in England in 1908. (Now a word of warning if you are going to try them. The Liberty puzzles are difficult. It can take weeks to complete one. I love that but it may not suit you). If I’m working on something and have writer’s block or need to clear my head – I find 10 minutes on a puzzle will work wonders. I go back to the task I am working on with a clearer head. In fact, this is nothing new. There has been a solid body of academic work showing the benefits of doing jigsaw puzzles in nurturing the creative power of the left side of the brain. This paper by Jan Gebers a good start if you’d like to explore more. However – in addition clearing one’s head, I’ve discovered a new truth in jigsaw puzzles that we can apply to other endeavours. This is the power of stepping away. I’ve found that sometimes I can spend 30 minutes trying to find the next piece of the Liberty puzzle I’m working on. And without success. It’s puzzle block! Then – if I step away and do something completely different for time – or go to bed – I’ve found that when I walk past later that day or next morning – often I will be able to place 4 or 5 pieces in rapid succession. Stepping away from the puzzle works wonders. So, if you are pondering a difficult challenge – maybe trying to finish that paper - or you are struggling to craft a suitable reply to a complex email – step away. Go and do something completely different, go for a walk or sleep on it until the next day. Make sure you physically step away. You’ll find that when you come back – your thoughts will flow and you’ll find those pieces. David L Thomas (also published on LinkedIn ) 4/2/2017 0 Comments What will competition, AI, block chain and automation do to Trade Finance? And some tips to thrive in the new world that’s dawning. I used the recent holiday period to sit back and explore some of the emerging global themes around my current professional area of banking practice, which is commodity and structured trade finance (CSTF) with corporate clients. We all know that growth in global trade has been weak. The trade finance departments in most of the world’s banks have been under significant pressure from weak transaction growth, or actual declines in business. Why is this and will it continue? Is there actually less business or is it going to the emerging non-bank competitors? We also know that block chain, artificial intelligence (AI), machine learning and cognitive intelligent systems will have a significant impact on traditional trade banking roles – especially document heavy processing areas in the so called “back office” functions. But how and where and how quickly? Finally, what should individual trade finance bankers do to thrive in the new world emerging in trade finance. I’ve collated some of my research into a deck you can download . These are my conclusions (2 minute read): 1. Global trade growth will continue be weak (probably around 1.5 – 2.5% over the next few years) – meaning traditional trade finance flows with the banking community will continue to be weak. Non–bank competitors will continue to take market share away from the global banks, who are under significant pressure to maintain acceptable return on risk weighted assets and to reduce exposure to higher risk geographies (which have increased in number). 2. To minimise the impact of the strong and agile non-bank competition emerging in the trade finance vacuum (the Asian Development Bank says the global un-met demand for trade finance is USD 1.6 trillion), banks will accelerate their investment in AI, block chain and distributed ledger systems and automation. This will lead to the exit of many traditional paper processing trade finance roles. 3. In my specific area of CSTF we will see an assertive entry by alternative funds who will be specifically targeting CSTF transactions with clients and in geographies that the global banks now find too difficult to operate (or the deals are simply too small to chase given the cost to service through regulation and compliance burdens). For a Trade Finance banker to thrive in the world that is dawning right now:

David L Thomas (also posted on LinkedIn ) 4/2/2017 0 Comments What will competition, AI, block chain and automation do to Trade Finance? And some tips to thrive in the new world that’s dawning.I used the recent holiday period to sit back and explore some of the emerging global themes around my current professional area of banking practice, which is commodity and structured trade finance (CSTF) with corporate clients.

We all know that growth in global trade has been weak. The trade finance departments in most of the world’s banks have been under significant pressure from weak transaction growth, or actual declines in business. Why is this and will it continue? Is there actually less business or is it going to the emerging non-bank competitors? We also know that block chain, artificial intelligence (AI), machine learning and cognitive intelligent systems will have a significant impact on traditional trade banking roles – especially document heavy processing areas in the so called “back office” functions. But how and where and how quickly? Finally, what should individual trade finance bankers do to thrive in the new world emerging in trade finance. I’ve collated some of my research into a deck you can download (be warned – it’s over 30 pages!). These are my conclusions (2 minute read):

David L Thomas |

Occasional updates and papers from Chartwell Consulting Pty LtdCharwell Consulting has a wide range of interests and activities across the areas of health, food, energy, water and metal - and the supply chains and investment channels for these sectors. Sometimes we post information we would like to share. Archives

June 2023

Categories |

RSS Feed

RSS Feed

Copyright © 2024